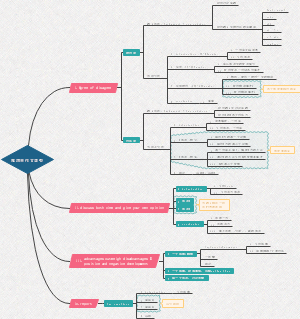

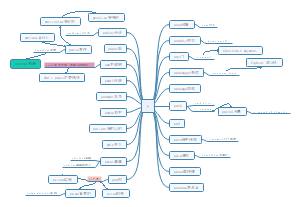

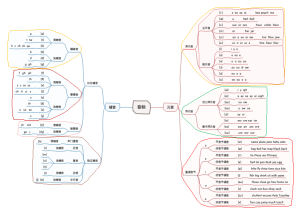

operational audits : systematic review of the efficiency and effectiviness of operation

finacial audit :financial informations are reliable and produced in an effecient and timely manner

the audit of IT systerms : procive a reliable basis and reducing risk of misstatements

compliance audit : compliance with law and regulations

fraud investgations: range from theft to assets to fraudulent financial reporting ;investigate specific instance of suspected fraud :review and test control and prevent or detect fraud .

customer experience audits :phoning in or visiting stores/outlets

Assessing the need for internal audit

scale and diversity of activities

cost /benenfit considerations

the desire of senior management to have assurance and advice on risk and control

the current control environment and whether there is a history of fraud or control deficiencies

internal audit & external audit

objective : improve operation and review efficiency // express an opinion

appointment : audit committee // shareholders

reporting : management and TCWG // publicli available to shareholders

responsibilities for fraud and error : prevention of fraud and error by assessing the effectiveness of internal control systerm.//obtaining reasonable assurance the FS are free from material misstatement whether caused by fraud or error.

outsouring internal audit function

Advantages

be independent of client // qualified ,competent staff , broader renge of expertise //specialist skills // flexible basis, more cost effective // new market place technologies // cost of permanent staff are avoidede

Disadvantages

lack the intimate knowledge of organisation // engagements are constrained by contractual terms // fees may be high // ethical threat // lack of control over the quality of service .

limitation of internal audit

employees of the company may not wish to raise issues// internal audit may be a part of the finance function // familiarity threat : long standing colleagues and friends