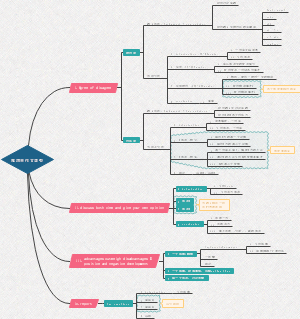

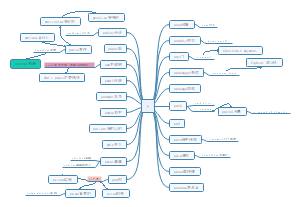

is to assist management in planning and controlling the resources of their organisation by providing appropriate control information

The importance of motivation

Behavioural problems

The managers who set the budget are not responsible for achieving it

Poor attitudes when setting the budget

Poor attitudes when putting plans into action

Control is applied at different stages by different people

Goal congruence

when individuals make decisions that are in their self-interest and also in the best interest of the organisation.

Dysfunctional decision-making

Participation in budgeting

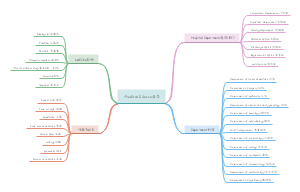

Top-down/imposed style budgeting

An imposed/top-down budget is set without allowing the budget holder to have the opportunity to participate in the budgeting process.

appropriate in

In newly formed organisations

During times of economic hardship

When operational managers lack budgeting skills

Bottom-up/participative budgeting

ensures all budget holders are given the opportunity to participate in setting their own budgets.

Advantages

Staff doing the work have the most accurate knowledge of operations

More achievable targets based on local knowledge

Morale and motivation improved as people are working towards their own budgets

Reduces the work load of top management

Disadvantages

Staff may set targets that are too easy and lack consistency (budgetary slack)

May never get agreement if too many conflicting views

Staff may lack skills/knowledge required

Performance evaluation

The key features of feedback

Clear and comprehensive reports

Reports identify controllable costs and revenues

Timely reports (eg so control action can be taken)

Style of evaluation Comment

Controllable vs uncontrollable costs

Managerial incentive schemes

Profit sharing schemes

Advantages

The company will only pay what it can afford out of actual profits.

Bonus can also be paid to non-production personnel.

Disadvantages

Employees must wait until the year end for a bonus(ie long-term commitment without the incentive of immediate reward).

Factors affecting profit may be outside the control of employees.

Too many employees involved in a single scheme may not have a great motivating effect on individuals.

Incentive schemes involving shares

Advantages

Employees feel they have a stake in the business.

·May offer incentive to employees to make decisions that focus on long-term benefits (rather than just short-term profits)

Disadvantage

·Benefits are not certain as the market value of shares cannot realistically be predicted.

·Benefits are not immediate, as a scheme must be in existence for several years before members can exercise their rights.

Value added incentive schemes

Value added=sales-cost of bought-in materials and services.

excludes any bought-in costs, and is affected only by costs incurred internally, such as labour.