导图社区 PPE

PPE

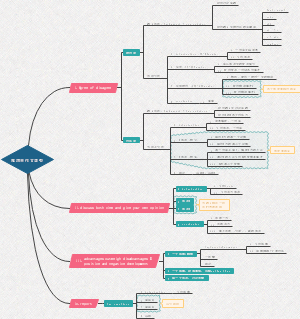

ACCA fr,内含有tangible asset、 recognition、 initial measurement。

编辑于2024-05-22 10:46:45- ACCA

- PPE

ACCA fr,内含有tangible asset、 recognition、 initial measurement。

- 10Costing methods

acca f2 第十章Costing methods,内容有: Job and batch costing Service costing Joint and by-products Activity-based costing (ABC) Total quality management(TQM) Life cycle costing Target costing

- 14Standard costing

acca f2 第14章, a control technique which compares standard costs and revenues with actual results. Differences between standard and actual results are called variances and these are used to improve performance.

PPE

社区模板帮助中心,点此进入>>

- PPE

ACCA fr,内含有tangible asset、 recognition、 initial measurement。

- 10Costing methods

acca f2 第十章Costing methods,内容有: Job and batch costing Service costing Joint and by-products Activity-based costing (ABC) Total quality management(TQM) Life cycle costing Target costing

- 14Standard costing

acca f2 第14章, a control technique which compares standard costs and revenues with actual results. Differences between standard and actual results are called variances and these are used to improve performance.

- 相似推荐

- 大纲