导图社区 Chapter 10Professional ethics

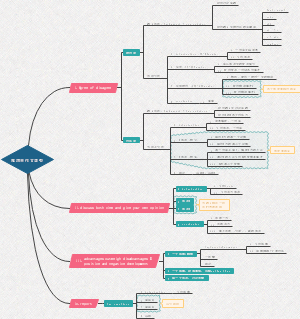

Chapter 10Professional ethics

ACCA BT, Ethics(伦理学) is the system of moral principles that examines the concept of right and wrong.伦理学是检验对与错的概念的道德原则体系。

编辑于2024-11-16 09:19:00- 伦理学

- 职业道德

- Chapter 6External Analysis

ACCA BT ,这张思维导图提供了一个全面而细致的外部分析框架,旨在帮助企业或组织识别和分析影响其运营的各种外部因素,从而制定出更加科学合理的战略和决策。

- Chapter 4information technolog

ACCABT,is data that has been processed in such a way that it has meaning to the person that receives it.已经过处理的数据,可用于做决定。

- Chapter 9Competitive Factors

ACCA BT ,包含organisation that affect its competitiveness:影响企业竞争力的活动、Porter’s Value Chain、SWOT Analysis SWOT分析等。

Chapter 10Professional ethics

社区模板帮助中心,点此进入>>

- Chapter 6External Analysis

ACCA BT ,这张思维导图提供了一个全面而细致的外部分析框架,旨在帮助企业或组织识别和分析影响其运营的各种外部因素,从而制定出更加科学合理的战略和决策。

- Chapter 4information technolog

ACCABT,is data that has been processed in such a way that it has meaning to the person that receives it.已经过处理的数据,可用于做决定。

- Chapter 9Competitive Factors

ACCA BT ,包含organisation that affect its competitiveness:影响企业竞争力的活动、Porter’s Value Chain、SWOT Analysis SWOT分析等。

- 相似推荐

- 大纲